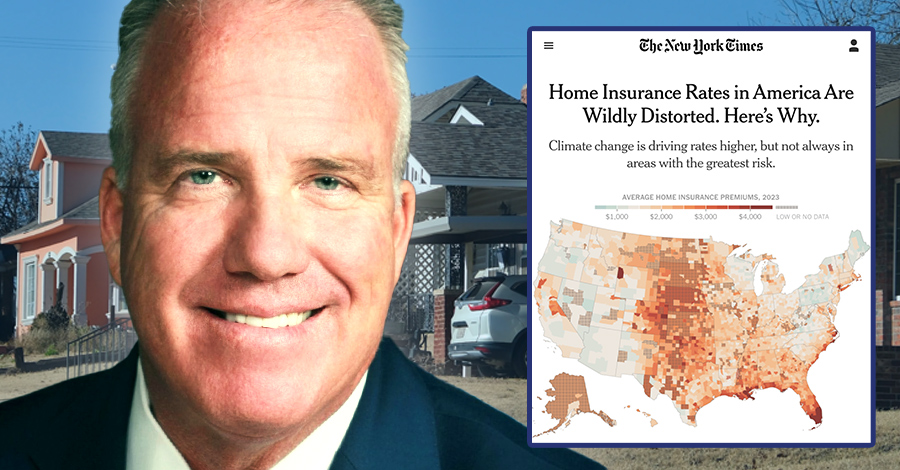

Last summer, the NY Times took a big look into rising home insurance rates across the country, and how despite people in different states sharing equal risks when it comes to claims, rates vary widely from state to state.

The primary conclusion from the investigation – which was backed by “woke” media things like data, research, and good reporting – is that residents stuck in low-regulatory states with spineless industry-controlled insurance commissioners like Oklahoma’s Glen Mulready are usually left paying higher premiums.

For example:

Oklahoma is the sixth-most expensive state for home insurance. (The top five are Florida, New York, Louisiana, Colorado and Hawaii.) But measured as a share of home value, Oklahoma ranks third, behind Louisiana and Mississippi.

Along the edges of Oklahoma, the premium paid by the typical household last year was as much as 70 percent higher than in adjacent counties in Texas, Arkansas and Kansas — despite those counties having similar levels of exposure to disasters, according to federal data.

Megann Johnson is an insurance agent in Enid whose own home insurance premiums almost doubled, to $4,860 this year from $2,570 in 2021. She says her aunts, who sell insurance in nearby Kansas, tease her about what they call Oklahoma’s “stupid” high rates. “Our risk is the same, right?” Ms. Johnson said. “We’re 50 miles from the state line.”

Glen W. Mulready, Oklahoma’s elected insurance commissioner, has never exercised his power to deny a rate increase requested by an insurance company for home insurance. He said he believed that competition, not regulation, was the best way to hold down prices.

I agree with Glen in that competition should keep prices down. But when it doesn’t – and a semi-commoditized product you’re basically required by law to carry keeps skyrocketing – maybe regulation isn’t the worst idea out there.

Then again, I’m not a bought-and-paid-for politician who essentially does lip service and PR for the insurance industry.

Earlier this week, Glen – now armed with ultra-long em-dashes, colons, and hollow points of ChatGPT – issued an editorial to various newspapers that defended his benevolence to insurance companies.

He basically wants you to know he doesn’t set rates, doesn’t approve rates, and doesn’t stop rates from skyrocketing — he just watches it all happen very legally.

Check this out:

Lately, there’s been growing concern — and even criticism — about rising homeowners' insurance rates in Oklahoma. I understand the frustration. Some have asked whether the Oklahoma Insurance Department, and I personally, are doing enough. So let me set the record straight.

First, let me tell you what the Oklahoma Insurance Department (OID) does regarding rates. Contrary to what some believe, we don’t set them. We don’t approve them. Oklahoma, like 37 other states, uses a “file-and-use” or “use-and-file” system. Our job is to ensure that those filings are lawful, non-discriminatory and transparent. We monitor the market closely, enforce consumer protections and act when companies break the law.

Yep, he doesn’t “approve” the rates. Notice how he didn’t mention that he doesn’t "disapprove" them either?

Like any good politician defending an industry that heavily donated to his campaign and got him elected, Glen made sure to stretch the truth and rely on played-up stereotypes to defend his industry’s pillage of Oklahomans’ money.

Now I want to talk about why rates are high, because they affect all of us. It’s not only because of hail! Oklahoma is one of the most disaster-prone states in the country. We face tornadoes, hail, wind, wildfires and floods — many times, all in the same year. These natural disasters have caused significant damage and massive payouts by insurance companies.

That’s cool and everything — if only it were true.

The @NYTimes highlights new research from Prof. @Key_Z_E & @UWBusiness Prof. @Philipcheesy1 on the rising cost of home insurance premiums in certain areas of the country due to climate change: https://t.co/vaImxcNHEA pic.twitter.com/upRsreB4wo

— The Wharton School (@Wharton) July 13, 2024

With out out of the way, let's get back to Mulready's spin offensive for the insurance industry:

In 2023, insurers in Oklahoma paid out $129 in claims for every $100 they collected in premiums. That kind of imbalance simply isn’t sustainable. Even after some improvement in 2024, payouts are still at $97 per $100 in premiums. When companies consistently lose money, they raise rates — some even stop writing new policies and leave the state. Luckily, we are not seeing an exodus of companies.

Oklahoma consumers have choices because of the way our state works. Over 100 licensed companies write homeowners insurance in Oklahoma, and more than 50 are actively doing so. Competition in the market helps keep prices in check.

Yep. Lucky us, huh? Insurance companies make such a killing in Oklahoma via unregulated competition that none of them want to leave!

If only there were a way we could shift money to their pals in the roofing and construction industry, they’ll make sure to keep those rates down. Wink wink.

OID is also pushing forward and working on long-term solutions. One example is the Strengthen Oklahoma Homes grant program, which helps homeowners fortify their homes against severe weather. Stronger homes mean fewer claims and lower premiums.

I do hear your concerns, and I share them. Nobody wants to see costs go up. But I want you to know this: Our team is fighting every day to ensure Oklahoma’s insurance market remains fair, competitive and focused on protecting you. That’s our mission. That’s our commitment.

I swear I’m not just trying to be a hail cloud heading toward a brand-new roof here, but after reading Glen’s article — and finding out my home insurance is going up again — I walked away with a slightly different take.

If you ask me, it kind of feels like Glen's mission and commitment is making sure Oklahoma’s insurance market remains fair, competitive, and focused on protecting insurance companies… not Oklahomans.

Stay with The Lost Ogle. We’ll keep you advised.